July 2026

Tech Companies’ Explosive Growth in Value Added Tops 2,000 Percent over 25 Years

An examination of value added—the measurement of an industry’s contribution to Gross Domestic Product (GDP)—shows that one sector has outpaced all others since 2000. Over the last quarter-century, the data processing, internet publishing, and other information services sector grew by more than half a trillion dollars, representing a staggering 2,050% increase. Consequently, the industry’s value-added share of total GDP rose from 0.3% in 2000 to 1.9% in 2025, driven by dynamic tech giants like Amazon, Microsoft, IBM, Meta, Alphabet, and Salesforce.

Other top-performing industries since 2000 include pipeline transportation, warehousing and storage, and transit and ground passenger transportation. The value added for each of these three sectors grew by approximately 400% over the same 25-year period.

Source: Bureau of Economic Analysis

June 2026

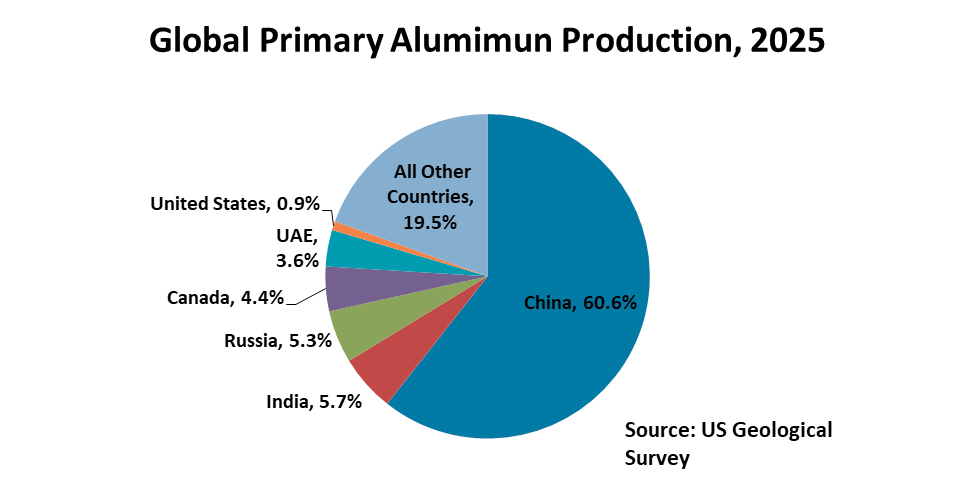

Can Trade Protections Save the U.S. Aluminum Industry?

Despite higher tariffs meant to boost domestic production and curb imports, the United States lags far behind China, which produces more than 60% of global primary aluminum. Other top producers include India, Russia, Canada, and the United Arab Emirates (UAE), who benefit from significantly lower energy costs.

U.S. Primary Aluminum Production

As of early 2025, just three companies operated the six remaining U.S. primary aluminum smelters, supporting approximately 59,000 jobs. The industry has recently announced plans to restart some idled capacity, while Century Aluminum and Emirates Global Aluminum are partnering to build the first major new U.S. smelter since 1980. Slated to break ground by late 2026 and begin production by the end of the decade, the facility, if built, is projected to produce 750,000 metric tons annually, more than doubling current U.S. output and adding 1,000 permanent direct jobs.

U.S. Secondary or Recycled Aluminum Production

In the meantime, the United States has increasingly pivoted toward secondary (recycled) aluminum, which now accounts for roughly 85% of domestic production (3.6 million metric tons) and requires far less energy. However, international competition is fierce, with China producing an estimated 40% of the global recycling supply.

Outlook

Trade protections and recycled aluminum can only do so much. While the commercial market relies heavily on secondary aluminum, advanced sectors like defense, aerospace, and electric vehicles (EVs) favor ultra-pure primary aluminum for critical systems. Following the sale and permanent closure of Century Aluminum’s Hawesville, Kentucky smelter in 2025 and 2026—previously the nation’s primary source for high-purity, military-grade aluminum—domestic manufacturers face a severe bottleneck. The United States now depends heavily on foreign primary aluminum, led overwhelmingly by Canada, with smaller shares from the UAE, Bahrain, and China.

Source: U.S. Geological Survey, Aluminum

May 2026

Canada Cedes to Mexico as Leading U.S. Export Market

In 2025, Mexico overtook Canada to become the leading destination for U.S. goods, according to the U.S. Census Bureau. Mexico now holds a lead of $8 billion, with its share accounting for 16% of all U.S. exports. This transition was driven by a 1% rise in shipments to Mexico, contrasted against a 6% decline in exports to Canada.

The Canadian Retreat

Trade with Canada faced a systemic downturn due to heightened tensions and supply chain disruptions. A $10 billion collapse in motor vehicle exports headlined the decline, followed by billion-dollar-plus decreases in fuels, plastics, and machinery. The impact also extended to the retail level, where actions by provincial liquor boards to delist U.S. products drove a $320 million deficit in American beverage exports.

Mexican Market Resilience

As a premier “nearshoring” hub, Mexico has deeply integrated into the U.S. industrial base. The “factory for the U.S.” model is a key driver of American export growth in sectors such as electrical and industrial machinery, energy, chemicals, and agriculture. However, this growth was partially offset by notable declines between 2024 and 2025. Leading these losses were a nearly $4 billion drop in fuel exports and an almost $3 billion decline in motor vehicles.

Outlook

The path forward for U.S.-Canada trade remains fraught with challenges. While a 2026 Supreme Court ruling struck down several emergency tariffs, the U.S.-Canada trade relationship remains under significant strain. Structural shifts are already underway; with Canadian firms aggressively diversifying their supply chains, trade volumes are unlikely to return to 2024 levels anytime soon.

Source: Department of Commerce, U.S. Census Bureau

April 2026

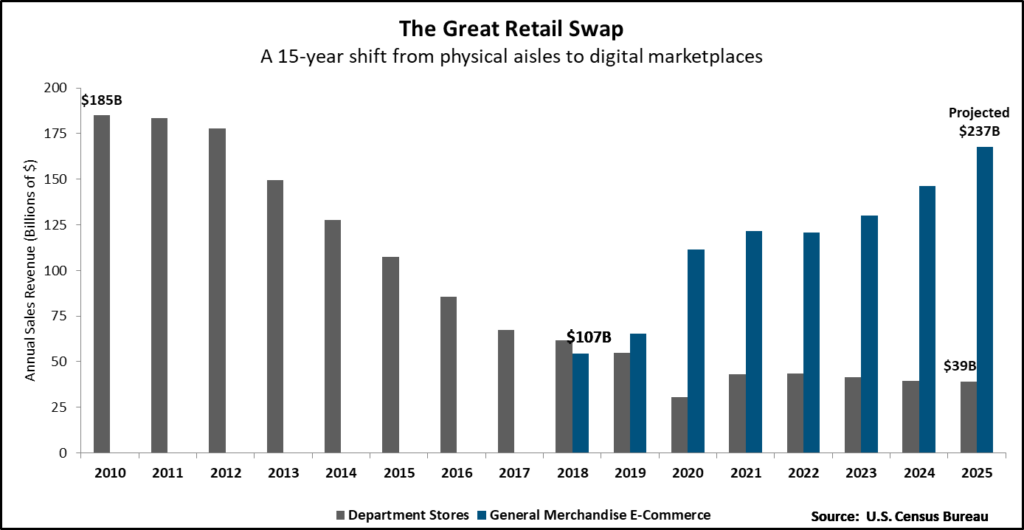

The Great Retail Swap: A New Reality

The department store’s reign as the primary engine of general merchandise sales is officially over—undone in just fifteen years by the very sector it once inspired. According to U.S. Census Bureau figures, brick-and-mortar department stores have seen nearly 80% of their annual revenue vanish, plummeting from $184.9 billion in 2010 to just $39.2 billion by the end of 2025.

As the number of physical stores thin out, the digital marketplace has claimed the crown. Clothing and general merchandise e-commerce is projected to hit $237 billion by the close of 2025— more than six times the earnings of its brick-and-mortar predecessors.

Source: Department of Commerce, U.S. Census Bureau

March 2026

Trump Slump Hits U.S. Tourism in 2025

The 2024 peak of 72 million visitors reversed in 2025 as a 5% total drop in foreign arrivals—termed the “Trump Slump”—took hold. Stricter vetting, new visa fees, and policy changes deterred travelers from key markets like Canada, Mexico, Europe, and Asia, redirecting them to global destinations with lower barriers to entry.

Reversing that trend won’t be easy. Despite the 2026 FIFA World Cup and America’s 250th anniversary, the One Big Beautiful Bill Act of 2025 slashed Brand USA funding by 80%. Why is the Trump Administration hollowing out its official travel promotion arm—originally secured through 2027—at the exact moment it is needed the most?

Source: Department of Commerce, U.S. Travel and Tourism Office

February 2026

Immigration: The U.S. Economy’s Secret Weapon

While the Trump Administration has consistently criticized the impact of foreign-born workers and moved to limit immigration—most notably through an overhaul of the H-1B nonimmigrant visa program—economic data suggests a different story. In fact, nearly one in five workers in the U.S. today was born abroad to non-citizen parents. This demographic grew to about 19.2% of the total U.S. labor force last year from 16.5% a decade ago. By the end of 2024, that came to 32.3 million people.

As shown in the table below, most of these foreign-born workers (over a third) were in management or professional roles, with another 20.0% in the service industry and 15.5% in production, transportation, and material moving occupations in 2024.

| Employment of Foreign-Born Workers by Occupation as a Percent of Total Employed | |||||

| Year | Management, Professional & Related Occupations | Service Occupations | Natural Resources, Construction and Maintenance Occupations | Production, Transportation and Material Moving Occupations | Sales and Office Occupations |

| 2014 | 30.7% | 24.1% | 13.7% | 15.6% | 16.0% |

| 2024 | 35.4% | 22.0% | 13.9% | 15.5% | 13.2% |

| Source: Bureau of Labor Statistics, Foreign–Born Workers: Labor Force Characteristics, 2024 | |||||

An analysis from the Federal Reserve suggests rising immigration has helped to address the recent shortfall in workers to fill the many job openings. By filling roles in construction and hospitality—sectors that faced severe shortages post-pandemic—immigrant labor has acted as a buffer against inflation and played a key role in preventing a major recession between 2024 and 2025.

Sources: Bureau of Labor Statistics and Federal Reserve Bank of Kansas City

January 2026

The Undersung Success of U.S. Services Sales

Washington policymakers often focus on the U.S. goods trade deficit, but it’s the nation’s services sector that remains a powerhouse of global commerce.

According to 2023 data from the Bureau of Economic Analysis, U.S.-based companies generated $3.05 trillion in services both through trade and through their foreign affiliates, significantly outperforming the $1.97 trillion in services imports and payments. Because many services require local delivery, the majority of these sales occur through foreign affiliates of U.S. multinational companies.

The United Kingdom was the primary market for these exports at $456 billion in 2023. Ireland ($328 billion) and Canada (over $250 billion) rounded out the top three U.S. services sales markets the same year.

Information services, wholesale trade, and finance and insurance represented the largest industry sectors in 2023.

However, this important economic engine faces growing risks because of the Trump Administration’s aggressive trade policy. These policies risk “tit-for-tat” retaliation from trading partners, introducing economic uncertainty and market instability, potentially stifling future growth in this critical sector.

Source: Bureau of Economic Analysis